MOTOSHARE 🚗🏍️

Rent Bikes & Cars Directly from Owners

Motoshare connects vehicle owners with people who need bikes and cars on rent. Owners earn from idle vehicles, and renters get flexible ride options.

Visit Motoshare

Introduction

Order-to-Cash platforms help businesses manage the full revenue collection journey, starting from customer orders and invoicing to payment collection, deductions, cash application, credit control, dispute handling, and reporting. In simple terms, these platforms help companies turn sales into collected cash faster, with fewer manual errors and better financial visibility.This matters because many finance teams still struggle with delayed payments, disconnected ERP data, manual reconciliation, invoice disputes, and poor collections prioritization. A strong Order-to-Cash platform can improve cash flow, reduce days sales outstanding, support compliance, and give finance leaders clearer control over receivables performance.

Real-world use cases include automated invoice delivery, customer credit risk monitoring, collections workflow management, payment reconciliation, dispute resolution, deduction management, cash forecasting, and shared-service finance operations.

Buyers should evaluate:

- End-to-end O2C coverage

- ERP and CRM integration depth

- Automation and AI capabilities

- Cash application accuracy

- Collections workflow flexibility

- Dispute and deduction management

- Reporting and analytics quality

- Security, access control, and audit readiness

- Scalability across regions and entities

- Implementation effort and change management

Best for: Order-to-Cash platforms are best for finance leaders, accounts receivable teams, shared service centers, CFO offices, credit managers, collections teams, and enterprises handling high invoice volumes. They are especially useful for mid-market and enterprise organizations in manufacturing, distribution, SaaS, healthcare, financial services, retail, logistics, telecom, and professional services.

Not ideal for: Very small businesses with simple invoicing needs may not need a full O2C suite. If a company only needs basic invoicing or payment links, accounting software or lightweight billing tools may be enough. Businesses with limited transaction volume, no complex collections process, and no ERP integration needs may find full O2C platforms too advanced or costly.

Key Trends in Order-to-Cash Platforms

- AI-driven collections prioritization: Modern O2C platforms increasingly use AI to identify high-risk accounts, recommend next-best actions, and prioritize collectors’ work based on payment behavior.

- Automated cash application: Finance teams are moving away from manual remittance matching toward automated cash application using machine learning, bank data, lockbox files, and ERP records.

- Customer self-service portals: More platforms now offer customer portals where buyers can view invoices, raise disputes, make payments, and download statements without emailing finance teams.

- Integrated credit risk management: Credit teams want real-time visibility into customer risk, payment history, credit limits, and exposure before approving new orders or extensions.

- Faster dispute and deduction resolution: Businesses are investing in tools that route disputes, deductions, and short payments to the right teams with clear audit trails.

- ERP-native and ERP-connected workflows: Strong integration with SAP, Oracle, Microsoft Dynamics, NetSuite, Salesforce, and major payment gateways is now a core buying requirement.

- Global shared services support: Large enterprises need multi-currency, multi-entity, multi-language, and regional compliance support for centralized finance operations.

- Predictive cash forecasting: O2C data is increasingly used to forecast incoming cash, model payment delays, and support treasury planning.

- Embedded payments and digital invoicing: Buyers expect digital payment options, automated reminders, and invoice delivery through multiple channels.

- Stronger audit and access controls: Role-based access, workflow approvals, audit logs, and configurable permissions are becoming essential for regulated and enterprise environments.

How We Selected These Tools

The tools below were selected using a practical buyer-focused evaluation approach:

- Market adoption and mindshare: Platforms widely recognized in finance transformation, accounts receivable automation, and enterprise O2C operations were prioritized.

- Feature completeness: Tools with broader coverage across invoicing, collections, cash application, deductions, disputes, credit, and analytics ranked higher.

- Enterprise readiness: Solutions suitable for complex finance teams, global operations, shared services, and multi-entity businesses were considered.

- Integration ecosystem: Platforms with strong ERP, CRM, banking, payment, and data integration capabilities were favored.

- Automation depth: Tools with AI, machine learning, workflow automation, and predictive analytics capabilities were evaluated positively.

- Scalability: Tools that can support growing invoice volumes, multiple business units, and complex customer portfolios were included.

- Security posture signals: Platforms offering enterprise access controls, audit logs, SSO, MFA, and permission management were considered stronger.

- Customer fit across segments: The list balances enterprise suites, mid-market platforms, AR automation tools, and specialized O2C providers.

- Reporting and visibility: Tools with dashboards, cash forecasting, aging analysis, and collector performance reporting were prioritized.

- Implementation practicality: Ease of deployment, onboarding support, documentation, and finance-team usability were considered.

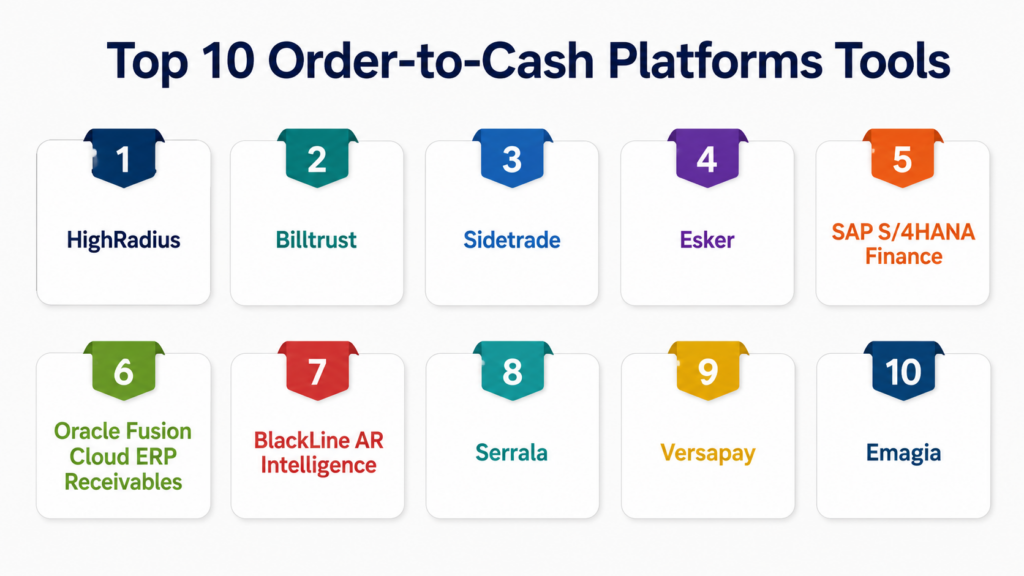

Top 10 Order-to-Cash Platforms Tools

#1 — HighRadius

Short description:

HighRadius is one of the most recognized platforms for autonomous finance and Order-to-Cash automation. It focuses heavily on accounts receivable, collections, credit, deductions, cash application, and treasury-related workflows. The platform is commonly used by large enterprises that want to reduce manual finance work and improve working capital visibility. It is especially strong for companies with large invoice volumes, complex customer portfolios, and global shared service teams.

Key Features

- AI-powered cash application and remittance matching

- Collections management with prioritized worklists

- Credit risk and credit limit management

- Deductions and dispute management workflows

- Electronic invoicing and payment support

- Dashboards for DSO, aging, disputes, and collector productivity

- Integration with major ERP and banking systems

Pros

- Strong end-to-end AR automation capabilities for large finance teams

- Good fit for enterprises with high transaction complexity

- AI and predictive analytics are central to the platform experience

Cons

- Implementation can require careful planning and business process alignment

- May be more advanced than what small businesses need

- Pricing and deployment effort may be significant for smaller teams

Platforms / Deployment

Web-based platform.

Cloud deployment.

Enterprise integrations vary by environment.

Security & Compliance

Enterprise access controls, role-based permissions, audit workflows, and secure integrations are commonly supported. Specific certifications may vary by contract and deployment, so buyers should validate current compliance documents during vendor review.

Integrations & Ecosystem

HighRadius is designed to connect with enterprise finance ecosystems, especially ERP, banking, and payment infrastructure. It is often used in complex environments where AR data needs to move between finance, customer, bank, and reporting systems.

- SAP

- Oracle

- Microsoft Dynamics

- NetSuite

- Banking and lockbox systems

- Payment gateways and remittance data sources

Support & Community

HighRadius typically supports enterprise onboarding, implementation services, training, documentation, and customer success programs. Support depth may vary by package, region, and contract tier.

#2 — Billtrust

Short description:

Billtrust is an Order-to-Cash and B2B payments platform focused on invoicing, payments, cash application, collections, and customer payment experiences. It is widely used by businesses that need to modernize accounts receivable and improve digital payment adoption. The platform is especially useful for companies that send high volumes of invoices and want customers to pay faster through digital channels. It combines AR automation with payment processing and customer-facing payment tools.

Key Features

- Digital invoicing and invoice delivery automation

- Online payment portal for B2B customers

- Automated cash application

- Collections workflow support

- Credit and risk-related capabilities

- Reporting for AR teams and finance leaders

- Integration with ERP and payment systems

Pros

- Strong B2B payments and invoice presentment capabilities

- Useful for improving customer payment experience

- Good fit for companies modernizing from paper-heavy AR processes

Cons

- Advanced configuration may require implementation support

- Some capabilities may depend on selected modules

- May not be ideal for companies needing only simple invoice creation

Platforms / Deployment

Web-based platform.

Cloud deployment.

Mobile access may vary by use case and configuration.

Security & Compliance

Billtrust supports enterprise security practices such as access controls, secure payment handling, and audit-friendly workflows. Buyers should validate current certifications, payment compliance requirements, and data protection documentation directly during procurement.

Integrations & Ecosystem

Billtrust integrates with ERP, accounting, payment, and banking environments to support invoice-to-payment workflows. Its ecosystem is especially relevant for companies that want digital invoice delivery and payment acceptance.

- ERP systems

- Accounting platforms

- Payment gateways

- Bank data sources

- Customer portals

- Lockbox and remittance sources

Support & Community

Billtrust offers onboarding, customer support, implementation assistance, and documentation. Support quality and service levels may vary depending on the selected plan and enterprise agreement.

#3 — Sidetrade

Short description:

Sidetrade is an AI-powered Order-to-Cash platform designed for finance teams that want to improve collections, reduce late payments, and automate customer payment behavior analysis. It focuses strongly on accounts receivable intelligence, collections prioritization, dispute workflows, and cash performance. Sidetrade is especially suitable for companies with large customer portfolios and distributed collections teams. Its AI-driven approach helps teams decide which accounts to contact, when to act, and how to improve payment outcomes.

Key Features

- AI-powered collections recommendations

- Customer payment behavior analysis

- Dispute and deduction workflow management

- Cash forecasting and receivables analytics

- Automated task management for collectors

- Customer risk segmentation

- Integration with ERP and finance systems

Pros

- Strong AI orientation for collections and receivables management

- Helpful for reducing manual prioritization work

- Good fit for large AR teams managing many customers

Cons

- Best value is achieved when historical AR data is available

- May require process changes for collections teams

- Not ideal for very small teams with limited invoice volume

Platforms / Deployment

Web-based platform.

Cloud deployment.

Global deployment options may vary by customer environment.

Security & Compliance

Sidetrade supports enterprise-grade access and data management practices. Specific certifications and compliance coverage should be confirmed directly during vendor evaluation.

Integrations & Ecosystem

Sidetrade connects with ERP and financial systems to analyze customer payment patterns and automate O2C workflows. It is typically used alongside existing finance systems rather than replacing core ERP.

- SAP

- Oracle

- Microsoft Dynamics

- ERP receivables modules

- Customer data sources

- Reporting and analytics tools

Support & Community

Sidetrade provides implementation guidance, customer success support, and documentation for finance teams. Support depth may vary by contract, region, and deployment complexity.

#4 — Esker

Short description:

Esker provides automation solutions for finance and customer service processes, including Order-to-Cash workflows such as order management, invoicing, collections, and payment handling. It is useful for companies that want to digitize manual document-heavy processes and improve operational efficiency. Esker is especially relevant for organizations that handle many customer orders, invoices, emails, and supporting documents. Its strengths include workflow automation, document processing, and integration with ERP systems.

Key Features

- Order management automation

- Invoice delivery and accounts receivable automation

- Collections management

- AI-assisted document capture and processing

- Customer communication workflow support

- Dashboards for finance and operations visibility

- ERP integration capabilities

Pros

- Strong document automation and workflow capabilities

- Useful for both finance and customer service teams

- Good fit for businesses with manual order and invoice processes

Cons

- Full value depends on workflow design and ERP integration quality

- May require configuration for complex business rules

- Some advanced features may depend on selected modules

Platforms / Deployment

Web-based platform.

Cloud deployment.

Hybrid integration patterns may be available depending on customer systems.

Security & Compliance

Esker supports enterprise access controls, workflow permissions, and secure process automation. Buyers should confirm current compliance certifications, regional data handling requirements, and audit controls during vendor review.

Integrations & Ecosystem

Esker integrates with ERP, email, document, and business systems to automate order and finance workflows. It is commonly used where incoming customer documents and outgoing finance documents need structured automation.

- SAP

- Oracle

- Microsoft Dynamics

- Email systems

- ERP order and finance modules

- Document capture and workflow systems

Support & Community

Esker provides implementation support, training, documentation, and customer services. Support experience may vary based on region, solution scope, and contract tier.

#5 — SAP S/4HANA Finance

Short description:

SAP S/4HANA Finance is a major enterprise finance platform that supports Order-to-Cash processes through integrated sales, billing, receivables, credit, collections, and financial reporting capabilities. It is best suited for large organizations already running or planning to run SAP as their core ERP. While it is broader than a standalone O2C tool, its deep integration across sales, logistics, finance, and accounting makes it highly relevant for enterprise O2C operations. Companies often extend SAP with specialized AR automation tools when they need more advanced collections or cash application.

Key Features

- Integrated billing and accounts receivable management

- Credit management and collections support

- Financial reporting and receivables visibility

- Integration with sales order and delivery processes

- Multi-entity and global finance capabilities

- Workflow and approval support

- Extensibility through SAP ecosystem tools

Pros

- Strong fit for large enterprises using SAP as the system of record

- Deep integration across sales, finance, logistics, and accounting

- Scalable for complex global finance operations

Cons

- Implementation and configuration can be complex

- Advanced AR automation may require additional modules or partner tools

- Less suitable for small companies without SAP infrastructure

Platforms / Deployment

Web and enterprise application access.

Cloud, on-premise, and hybrid deployment options may be available depending on SAP environment and edition.

Security & Compliance

SAP environments commonly support enterprise controls such as role-based access, audit logs, SSO, identity management, and compliance workflows. Specific certifications, controls, and regulatory coverage depend on deployment model and customer configuration.

Integrations & Ecosystem

SAP S/4HANA Finance has a broad enterprise ecosystem and can integrate with sales, procurement, supply chain, banking, analytics, tax, and AR automation tools. It often serves as the financial system of record for large organizations.

- SAP Sales and Distribution

- SAP Treasury and Cash Management

- SAP Analytics tools

- Banking integrations

- Third-party AR automation platforms

- Enterprise data platforms

Support & Community

SAP has a large global partner ecosystem, documentation base, implementation partner network, and enterprise support model. Support depends on licensing, partner engagement, and deployment type.

#6 — Oracle Fusion Cloud ERP Receivables

Short description:

Oracle Fusion Cloud ERP Receivables supports enterprise Order-to-Cash operations through billing, receivables, collections, customer account management, revenue processes, and financial reporting. It is best suited for organizations using Oracle Cloud ERP as their finance backbone. The platform helps finance teams manage customer invoices, receipts, adjustments, collections, and accounting in a centralized cloud environment. It is especially relevant for large and mid-market companies that want strong ERP-native O2C capabilities.

Key Features

- Accounts receivable and customer billing management

- Receipt processing and cash application support

- Collections and customer account workflows

- Financial reporting and receivables analytics

- Credit and customer account visibility

- Multi-entity and multi-currency finance support

- Integration with Oracle Cloud ecosystem

Pros

- Strong fit for Oracle ERP customers

- Broad finance and accounting capabilities beyond standalone AR

- Scalable for multi-entity and enterprise finance operations

Cons

- May require Oracle ecosystem alignment for best value

- Implementation can be complex for large organizations

- Specialized AR automation may require complementary tools

Platforms / Deployment

Web-based enterprise application.

Cloud deployment.

Mobile access may vary by Oracle application configuration.

Security & Compliance

Oracle Cloud environments commonly support enterprise security controls such as identity management, access controls, encryption, audit logging, and compliance-oriented administration. Buyers should validate current compliance details based on region, product edition, and contract.

Integrations & Ecosystem

Oracle Fusion Cloud ERP Receivables integrates across Oracle finance, procurement, sales, analytics, and reporting ecosystems. It can also connect with banking, tax, payment, and third-party AR automation tools.

- Oracle Cloud ERP

- Oracle Financials

- Oracle Analytics

- Banking systems

- Payment processors

- Third-party finance applications

Support & Community

Oracle provides enterprise support, documentation, training resources, and partner implementation services. Support quality depends on subscription level, implementation partner, and internal Oracle expertise.

#7 — BlackLine AR Intelligence

Short description:

BlackLine is well known for financial close and accounting automation, and its accounts receivable capabilities support cash application, collections, credit, disputes, and AR intelligence. BlackLine AR Intelligence is useful for finance teams that want better visibility into receivables, customer risk, and cash performance. It is often considered by companies already investing in finance automation and close optimization. The platform is strong for improving control, accuracy, and visibility across finance operations.

Key Features

- Cash application automation

- Collections and customer account prioritization

- AR analytics and performance dashboards

- Dispute and deduction workflow support

- Customer risk and receivables visibility

- Finance automation and accounting workflow alignment

- Integration with ERP and banking systems

Pros

- Strong finance automation brand with broad accounting relevance

- Useful for improving visibility and control across AR processes

- Good fit for companies already using BlackLine for finance transformation

Cons

- May be more finance-control oriented than customer-payment focused

- Best results require strong ERP and bank data integration

- May need careful module selection for full O2C coverage

Platforms / Deployment

Web-based platform.

Cloud deployment.

Enterprise integration options vary by customer environment.

Security & Compliance

BlackLine commonly supports enterprise security practices such as role-based access, audit trails, secure workflows, and administrative controls. Specific certifications and compliance status should be verified during procurement.

Integrations & Ecosystem

BlackLine integrates with ERP, banking, and finance systems to support accounting automation and receivables workflows. It is often deployed alongside large ERP platforms.

- SAP

- Oracle

- Microsoft Dynamics

- Banking data sources

- ERP receivables modules

- Finance reporting systems

Support & Community

BlackLine offers enterprise support, customer success resources, documentation, and implementation services. Community and partner support are stronger in enterprise finance automation environments.

#8 — Serrala

Short description:

Serrala is a finance automation platform with capabilities across Order-to-Cash, payments, cash management, treasury, and working capital processes. It is especially relevant for enterprises that want to connect AR automation with broader cash and treasury workflows. Serrala supports cash application, collections, dispute management, payment processes, and financial automation. It is often used by companies with complex SAP-centric or enterprise finance environments.

Key Features

- Cash application automation

- Collections and dispute management

- Payments and treasury process support

- Working capital and cash visibility

- AR reporting and analytics

- Enterprise workflow automation

- Strong integration focus with ERP systems

Pros

- Good fit for enterprise finance and treasury-connected O2C processes

- Strong relevance for complex ERP environments

- Useful for organizations looking beyond basic AR automation

Cons

- May be more complex than needed for simple AR teams

- Implementation scope can grow if treasury and payments are included

- Buyers should carefully validate module fit before selection

Platforms / Deployment

Web-based and enterprise application access.

Cloud, hybrid, or ERP-connected deployment patterns may vary by solution and customer environment.

Security & Compliance

Serrala supports enterprise finance security requirements such as access controls, workflow governance, and audit-friendly process management. Specific certifications and compliance details should be validated directly with the vendor.

Integrations & Ecosystem

Serrala integrates with ERP, banking, treasury, payment, and finance systems. It is particularly relevant where receivables and cash operations need to be connected.

- SAP

- Oracle

- Banking platforms

- Treasury systems

- Payment networks

- Finance reporting tools

Support & Community

Serrala provides enterprise implementation, documentation, onboarding, and customer support. Support depth may vary by region, module scope, and service agreement.

#9 — Versapay

Short description:

Versapay is a collaborative accounts receivable and payment platform focused on helping companies invoice, collect, communicate, and accept payments from customers. It is especially useful for businesses that want to improve customer collaboration around invoices and reduce back-and-forth email communication. Versapay combines AR automation with digital payment acceptance and customer self-service. It is a strong fit for mid-market and enterprise teams that want better invoice visibility and faster customer payments.

Key Features

- Online invoice presentment and payment portal

- Customer collaboration around invoices and disputes

- Accounts receivable automation

- Collections communication workflows

- Payment processing support

- Cash application and reconciliation support

- AR visibility and reporting dashboards

Pros

- Strong customer-facing invoice and payment experience

- Useful for reducing manual AR communication

- Good fit for companies wanting collaborative payment workflows

Cons

- Full O2C depth may depend on selected modules and integrations

- May not replace broader ERP finance functions

- Advanced enterprise needs may require complementary systems

Platforms / Deployment

Web-based platform.

Cloud deployment.

Mobile access may vary by configuration.

Security & Compliance

Versapay supports secure payment and AR workflows. Buyers should confirm current security certifications, payment compliance requirements, access controls, and data protection documentation during vendor review.

Integrations & Ecosystem

Versapay integrates with ERP, accounting, payment, and customer systems to support invoice-to-payment collaboration. Its ecosystem is strongest where AR teams need both customer portals and payment automation.

- ERP systems

- Accounting platforms

- Payment processors

- Customer portals

- Bank and remittance data

- Reporting systems

Support & Community

Versapay offers onboarding, documentation, implementation assistance, and customer support. Support levels may vary by plan, deployment complexity, and integration scope.

#10 — Emagia

Short description:

Emagia is an AI-powered Order-to-Cash platform focused on autonomous receivables, collections, credit, deductions, cash application, and customer finance operations. It is designed for organizations that want to use automation and analytics to improve AR performance. Emagia is especially relevant for finance teams handling large customer bases, high invoice volumes, and complex payment behavior. Its platform aims to bring intelligence and automation across the receivables lifecycle.

Key Features

- AI-assisted collections management

- Cash application automation

- Credit management workflows

- Deductions and dispute handling

- Customer payment behavior analytics

- Receivables dashboards and reporting

- ERP and finance system integrations

Pros

- Strong focus on AI-powered receivables automation

- Covers multiple parts of the O2C lifecycle

- Useful for finance teams seeking predictive insights

Cons

- Requires good AR data quality for best outcomes

- May require implementation support for complex workflows

- Smaller teams may not need the full platform depth

Platforms / Deployment

Web-based platform.

Cloud deployment.

Integration options vary by customer environment.

Security & Compliance

Emagia supports enterprise finance workflows and access control expectations. Specific compliance certifications and security documentation should be confirmed directly during vendor evaluation.

Integrations & Ecosystem

Emagia connects with ERP, banking, payment, and finance systems to support receivables automation. It is commonly evaluated by teams that want AI-driven workflows layered over existing systems.

- SAP

- Oracle

- Microsoft Dynamics

- Banking systems

- Payment data sources

- ERP receivables modules

Support & Community

Emagia provides implementation support, training, documentation, and customer success resources. Support availability and depth may vary by contract and deployment scope.

Comparison Table

| Tool Name | Best For | Platform(s) Supported | Deployment | Standout Feature | Public Rating |

|---|---|---|---|---|---|

| HighRadius | Large enterprises and shared services | Web | Cloud | AI-powered AR and cash application automation | N/A |

| Billtrust | B2B invoicing and payments | Web | Cloud | Digital invoice delivery and payment portal | N/A |

| Sidetrade | AI-driven collections teams | Web | Cloud | Predictive collections prioritization | N/A |

| Esker | Document-heavy O2C workflows | Web | Cloud | Order and invoice workflow automation | N/A |

| SAP S/4HANA Finance | SAP-centric enterprises | Web / Enterprise apps | Cloud / Hybrid / On-premise options vary | ERP-native finance and O2C integration | N/A |

| Oracle Fusion Cloud ERP Receivables | Oracle ERP customers | Web | Cloud | Integrated receivables inside Oracle Cloud ERP | N/A |

| BlackLine AR Intelligence | Finance automation and AR visibility | Web | Cloud | AR intelligence and cash application support | N/A |

| Serrala | Enterprise finance and treasury-connected O2C | Web / Enterprise apps | Cloud / Hybrid options vary | Receivables connected with payments and cash operations | N/A |

| Versapay | Customer payment collaboration | Web | Cloud | Collaborative AR portal and digital payments | N/A |

| Emagia | AI-powered receivables automation | Web | Cloud | Autonomous receivables and O2C intelligence | N/A |

Evaluation & Scoring of Order-to-Cash Platforms

The scoring below is comparative and based on category fit, feature breadth, ecosystem strength, enterprise readiness, and practical buyer value. It is not a universal ranking for every company. A platform with a lower score may still be the best choice if it fits your ERP, budget, region, or workflow better.

| Tool Name | Core (25%) | Ease (15%) | Integrations (15%) | Security (10%) | Performance (10%) | Support (10%) | Value (15%) | Weighted Total (0–10) |

|---|---|---|---|---|---|---|---|---|

| HighRadius | 9.5 | 8.0 | 9.0 | 8.5 | 9.0 | 8.5 | 8.0 | 8.75 |

| Billtrust | 8.7 | 8.5 | 8.5 | 8.0 | 8.5 | 8.0 | 8.3 | 8.43 |

| Sidetrade | 8.8 | 8.3 | 8.2 | 8.0 | 8.5 | 8.0 | 8.1 | 8.36 |

| Esker | 8.5 | 8.4 | 8.4 | 8.0 | 8.3 | 8.1 | 8.0 | 8.31 |

| SAP S/4HANA Finance | 9.0 | 7.2 | 9.5 | 9.0 | 9.0 | 8.5 | 7.4 | 8.50 |

| Oracle Fusion Cloud ERP Receivables | 8.8 | 7.6 | 9.0 | 9.0 | 8.8 | 8.4 | 7.6 | 8.43 |

| BlackLine AR Intelligence | 8.3 | 8.2 | 8.5 | 8.5 | 8.4 | 8.3 | 7.9 | 8.28 |

| Serrala | 8.4 | 7.8 | 8.7 | 8.4 | 8.4 | 8.0 | 7.8 | 8.23 |

| Versapay | 8.0 | 8.7 | 8.0 | 8.0 | 8.2 | 8.0 | 8.4 | 8.21 |

| Emagia | 8.4 | 8.0 | 8.2 | 8.0 | 8.3 | 7.8 | 8.0 | 8.16 |

These scores should be interpreted as a structured comparison, not as fixed market ratings. A company already using SAP may find SAP S/4HANA Finance more practical than a standalone AR tool. A mid-market company focused on customer payments may get faster value from Billtrust or Versapay. Enterprises with high invoice volumes and complex collections may prefer HighRadius, Sidetrade, Serrala, or Emagia. Always validate integrations, security documentation, implementation effort, and total cost before making a final decision.

Which Order-to-Cash Platforms Tool Is Right for You?

Solo / Freelancer

Solo professionals and freelancers usually do not need a full Order-to-Cash platform. Their needs are typically limited to invoice creation, payment reminders, basic accounting, and payment links. A lightweight accounting or invoicing tool is usually a better fit than enterprise O2C software.

However, freelancers working with many corporate clients may still benefit from basic receivables automation. In that case, they should prioritize simple invoicing, payment tracking, reminder automation, and low-cost payment acceptance rather than advanced credit, deductions, and ERP workflows.

SMB

Small and mid-sized businesses should look for ease of use, fast implementation, invoice automation, payment portals, and basic collections workflows. Billtrust, Versapay, and Esker can be strong options depending on invoice volume, customer payment behavior, and integration needs.

SMBs should avoid overbuying. A platform with too many enterprise modules can slow implementation and increase cost. The best option is often one that improves invoice delivery, customer payments, reminders, and reconciliation without requiring major finance transformation.

Mid-Market

Mid-market companies often need stronger O2C automation because invoice volume, customer complexity, and collections pressure increase as the business grows. These companies should evaluate Billtrust, Versapay, Esker, Sidetrade, BlackLine, and Emagia depending on their priorities.

If the biggest issue is delayed payments, collections intelligence matters. If the main challenge is manual invoice delivery, invoice presentment and payment portals matter more. If reconciliation is the bottleneck, cash application automation should be the top requirement.

Enterprise

Enterprises should prioritize scalability, global support, ERP integration, security controls, workflow flexibility, and analytics. HighRadius, SAP S/4HANA Finance, Oracle Fusion Cloud ERP Receivables, Serrala, Sidetrade, and BlackLine are commonly relevant for this segment.

Large companies should also evaluate how the platform supports shared services, multiple business units, currencies, approval rules, dispute routing, and audit requirements. For many enterprises, the best architecture combines a core ERP with specialized O2C automation.

Budget vs Premium

Budget-conscious buyers should begin with the biggest pain point: invoicing, collections, cash application, or customer payments. Buying a full suite without clear process priorities can increase cost and delay value.

Premium platforms are better suited for organizations with high invoice volume, complex customer segments, multiple ERPs, global operations, and measurable working capital goals. The return is strongest when automation reduces manual workload, lowers DSO, and improves cash visibility.

Feature Depth vs Ease of Use

Feature-rich platforms offer deeper automation, advanced analytics, and more complex workflow options. However, they may require longer implementation and more training.

Ease-of-use platforms are better for teams that need faster adoption and simpler workflows. Buyers should choose based on internal maturity. A smaller AR team may prefer simple dashboards and automated reminders, while a large shared service center may need deep role-based workflows and advanced analytics.

Integrations & Scalability

Order-to-Cash platforms must connect well with ERP, CRM, billing, banking, payment, tax, and reporting systems. Weak integrations can create duplicate work and reduce automation value.

Before choosing a platform, buyers should map required integrations carefully. Key systems often include SAP, Oracle, Microsoft Dynamics, NetSuite, Salesforce, bank portals, payment gateways, lockbox files, data warehouses, and customer portals.

Security & Compliance Needs

Security matters because O2C platforms handle customer records, invoices, bank data, payment details, credit information, disputes, and financial transactions. Buyers should review SSO, MFA, RBAC, encryption, audit logs, data retention, regional hosting, and administrative controls.

Regulated industries should go further and validate compliance documentation, vendor risk reports, data processing terms, and access governance. Security should not be treated as a final checklist item; it should be part of early vendor screening.

Frequently Asked Questions

1. What is an Order-to-Cash platform?

An Order-to-Cash platform helps businesses manage the process from receiving a customer order to collecting payment. It may include invoicing, accounts receivable, collections, payment processing, dispute management, credit management, and cash application. The goal is to reduce manual work, improve cash flow, and give finance teams better visibility into receivables. In larger companies, O2C platforms often connect with ERP, CRM, banking, and payment systems. They are especially valuable when invoice volumes are high or collections processes are complex.

2. How is Order-to-Cash different from Quote-to-Cash?

Quote-to-Cash usually starts earlier in the revenue process, covering quoting, pricing, contract creation, order capture, billing, and revenue operations. Order-to-Cash begins once an order is placed and continues through invoicing, receivables, collections, payment, and reconciliation. In simple terms, QTC focuses on converting a sales quote into a booked and billed transaction, while O2C focuses on turning an order into collected cash. Some enterprise platforms overlap across both areas. Buyers should define their process scope before selecting a tool.

3. What pricing models do Order-to-Cash platforms usually use?

Most O2C platforms use subscription pricing, enterprise licensing, usage-based pricing, module-based pricing, or custom contract pricing. Pricing often depends on invoice volume, number of users, modules selected, ERP integrations, regions, and implementation complexity. Some vendors may charge separately for implementation, support, payment processing, or premium integrations. Buyers should not compare only license cost. They should compare total cost of ownership, including setup, training, integrations, data migration, and long-term administration.

4. How long does implementation usually take?

Implementation time depends on company size, ERP complexity, data quality, number of modules, and workflow customization. A focused deployment for invoice delivery or collections automation may be faster than a full enterprise O2C transformation. Large implementations involving ERP integration, cash application, disputes, credit, payments, and multiple regions can take longer. The biggest delays often come from unclear processes, poor master data, and incomplete integration planning. Buyers should run a phased rollout rather than trying to automate every workflow at once.

5. What are the most common mistakes when choosing an O2C platform?

A common mistake is buying the most feature-rich platform without defining the main business problem. Another mistake is underestimating ERP integration, data cleanup, and process redesign. Some teams also ignore collector adoption, customer payment experience, and dispute ownership. O2C automation works best when finance, sales, customer service, IT, and treasury teams align. Buyers should document current pain points, target outcomes, required integrations, approval rules, and reporting needs before vendor selection.

6. Are Order-to-Cash platforms secure?

Order-to-Cash platforms can be secure, but buyers must validate each vendor carefully. These platforms handle sensitive customer, invoice, payment, and financial data, so access control and auditability are important. Buyers should evaluate SSO, MFA, role-based permissions, encryption, audit logs, data retention, and administrator controls. They should also review vendor security documentation and compliance posture. Security requirements may differ depending on industry, geography, payment methods, and internal risk policies.

7. Can O2C platforms integrate with ERP systems?

Yes, ERP integration is one of the most important requirements for Order-to-Cash platforms. Most serious O2C tools are designed to connect with systems such as SAP, Oracle, Microsoft Dynamics, NetSuite, and other finance platforms. Integration may include customer master data, invoices, payments, credit memos, disputes, remittance files, and accounting entries. Buyers should validate whether integrations are prebuilt, API-based, file-based, or custom. The quality of integration often determines how much automation value the business receives.

8. Do these platforms support AI and automation?

Many modern O2C platforms include AI or machine learning features, especially for cash application, collections prioritization, payment prediction, dispute routing, and customer risk scoring. AI can help finance teams identify which accounts need attention, match payments to invoices, and forecast incoming cash. However, AI performance depends heavily on clean data, historical payment behavior, and proper workflow setup. Buyers should ask vendors to demonstrate AI features using realistic scenarios. They should also check whether users can explain, override, and audit automated recommendations.

9. When should a company switch from spreadsheets to an O2C platform?

A company should consider switching when spreadsheets create delays, errors, duplicate work, or poor visibility. Warning signs include late payment follow-ups, manual cash matching, unclear dispute ownership, aging reports that are always outdated, and collections teams working without prioritization. If finance leaders cannot accurately forecast incoming cash or understand customer payment risk, a dedicated platform may be needed. The switch becomes more urgent as invoice volume, customer count, and regional complexity grow. A phased rollout can reduce disruption.

10. What alternatives exist if we do not need a full O2C platform?

Alternatives include accounting software, invoicing tools, payment gateways, ERP receivables modules, CRM billing add-ons, and spreadsheet-based workflows. Small businesses may only need simple invoicing and payment reminders. Companies already using a strong ERP may extend native receivables features before buying a specialist tool. However, alternatives may become limiting when collections, disputes, cash application, and multi-entity reporting become complex. The right choice depends on transaction volume, customer complexity, integration needs, and finance maturity.

Conclusion

Order-to-Cash platforms play a critical role in helping businesses convert revenue into collected cash with better speed, accuracy, and control. The best platform depends on business size, invoice volume, ERP environment, payment complexity, customer behavior, and finance team maturity. HighRadius, Sidetrade, Serrala, Emagia, and BlackLine are strong options for organizations seeking deeper AR automation and intelligence, while Billtrust and Versapay are especially useful for digital invoicing, payments, and customer collaboration. SAP S/4HANA Finance and Oracle Fusion Cloud ERP Receivables are strong choices for companies already committed to those ERP ecosystems, and Esker is a practical fit for document-heavy order and invoice workflows. There is no single universal winner because each company has different process gaps, budget limits, integration needs, and compliance expectations.

Adopting comprehensive revenue lifecycle automation software optimizes commercial enterprise transactional fulfillment logistics, ensuring accelerated customer invoice settlement tracking and seamless corporate financial reconciliation workflows.